The Case for LATAM

Financial market returns across Latin America (LATAM) have been largely lackluster for the last decade. However, the world is changing. Covid-19, the war in Ukraine and increasing de-globalisation are inflationary forces in the world. This situation presents an opportunity for LATAM, and the future performance of their markets.

- Policy rates are between 11-14% in the region. Inflation is expected to come back to 5-6% in most countries in 2H, 23. Economic growth in the region will improve as Central Banks cut rates across the region in 2023-2024.

- The region is especially rich in key commodities for the upcoming Net zero energy transition. It plays a vital role in global food supply. At Ox, we believe it is critical for investors to gain exposure to the region as insurance against an inflationary world.

- The region represents 1% of the world index, but its importance to the world is vastly under appreciated by investors. At Ox, we see many exciting long duration investment opportunities available.

1. Background – A Significant Population, Emerging from the Pandemic Stronger

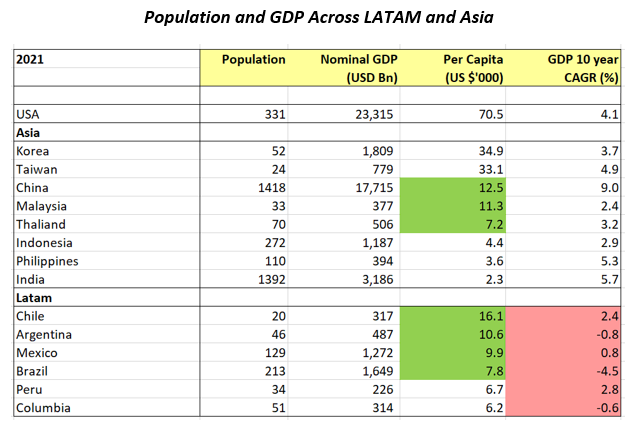

LATAM has a total population of over 650m. This is similar in size to ASEAN. However, GDP of US$5.3tr in 2021 for LATAM is over 50% larger than the ASEAN countries. Key countries of LATAM are reasonably wealthy compared with Asian ones, for example GDP per capita in Mexico, Argentina and Chile were ~US$16k, ~US$11k and US$10k respectively in 2021, compared with China at ~US$13k. LATAM has been trailing behind Asia in terms of GDP growth in recent times, with a relatively slower rate of growth over the past decade.

The five largest economies in the region are: Brazil (32% of LATAM GDP), Mexico (22%), Argentina (8%), Colombia (6%), and Chile (5%), equating to almost 75% of the region’s GDP. One of the reasons behind the region’s lagging growth over the past decade has been its under- representation in global trade, in an era of increasing globalization. Brazil and Argentina remain two of the most closed economies in the world, with trade only amounting to 30% of GDP, far below the global average of 52%.

Looking back over previous decades, the key barriers were lack of investment in good quality infrastructure, education, and governance. Logistics and transport infrastructure were underdeveloped across in the region, inhibiting efficient flow of goods and services. At times, there has been a significant skills gap between employers’ needs and the capabilities of the workforce, especially in relation to a shortage of engineers and technical staff. Finally, the region is known for its bureaucracy, red tape, and complex tax systems.

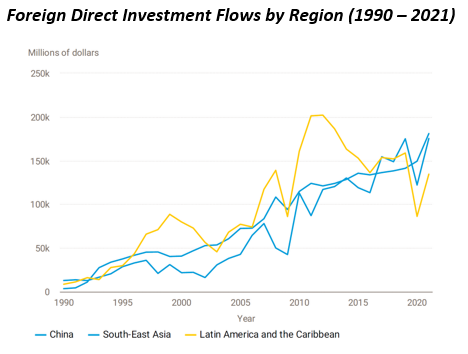

Despite its various weaknesses, LATAM remains a prospective destination for foreign direct investment (FDI). With FDI, some of the weaknesses have gradually improved. For a long time, LATAM had greater FDI inflows than even China and Southeast Asia respectively!

Given LATAM is a resource-rich region with a rising middle class and is short on efficient transportation infrastructure, the key recipient industries of FDI were that of natural resources (energy, base metals and agriculture), manufacturing (automotive, electronics, and aerospace), services (finance, telecommunications, and tourism), and logistics infrastructure.

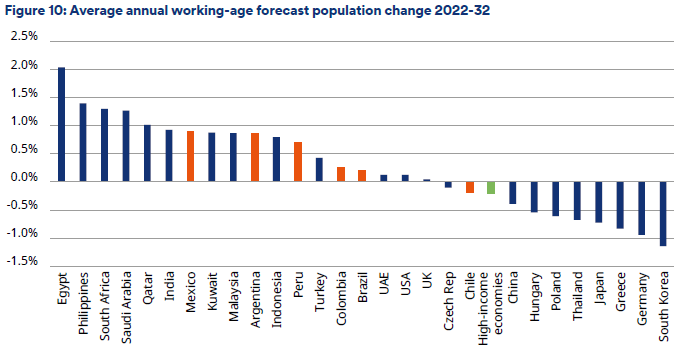

Demographics of the region is indeed favorable, as the middle-class population is expected to add 120M people by 2040 and the working age population will continue to grow.

Education standards are gradually improving. Take Brazil for example, the government increased its investment in education, with the share of GDP spent on education increased from 4.6% in 2000 to 6.0% in 2018. As a result, the literacy rate in Brazil has increased from 88.4% in 2000 to 93.2% in 2018 and school completion rates have increased over the last decade. Despite these improvements, there is still a significant disparity of education levels that exists between different socioeconomic backgrounds.

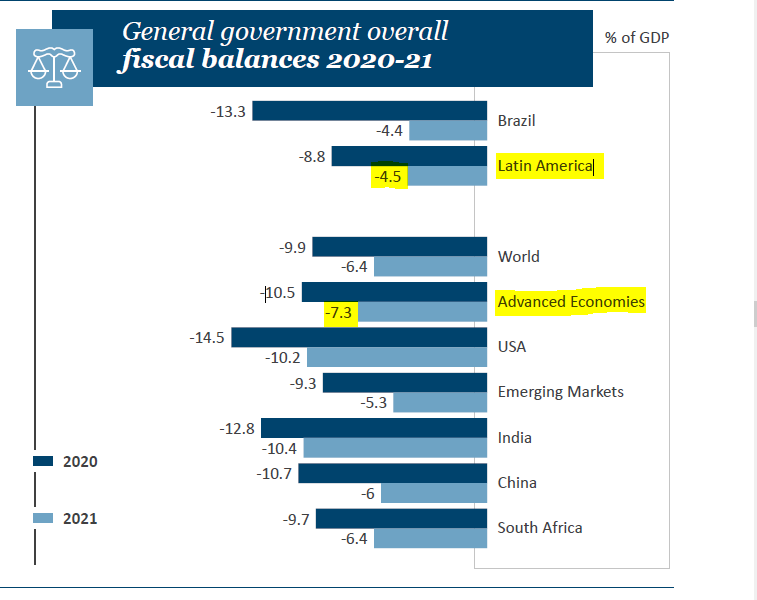

Key governments of the region have become more fiscally responsible in recent years. This was evident particularly during the pandemic, in which government spending was well controlled. For example, the average fiscal deficits in the region were -4.5% of GDP in 2021, more responsible than that of advanced economies at -7.3%. Furthermore, even the most indebted Government in LATAM, Brazil, only has government debt to GDP at 88%, which is lower than that of most developed country governments, including France (92%), Italy (147%), Japan (221%), UK (103%), and USA (115%).

2. LATAM : A Key Global Food and Minerals Supplier

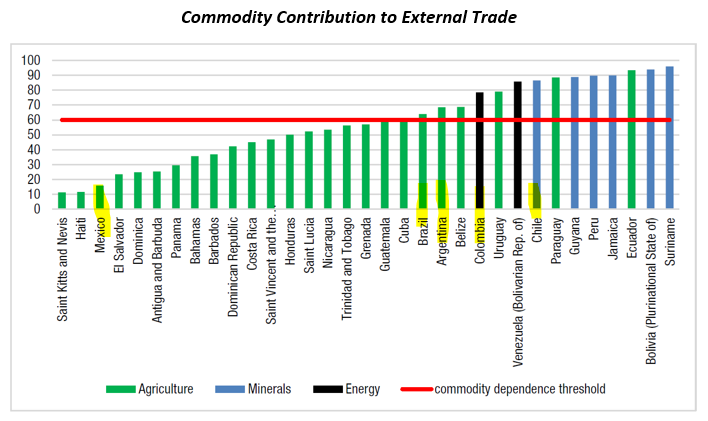

The LATAM region has an amazingly abundant endowment of natural resources. Commodity exports make up 60-90% of the region’s external trade which has driven wealth levels of the major economies – Chile at ~$16k per person and Argentina at ~$11k per person. As developing countries, particularly in Asia, continue to grow, demand for resources will continue to intensify. Given their large exposure to scarce resources, LATAM will be a key supplier and benefit from this disproportionately.

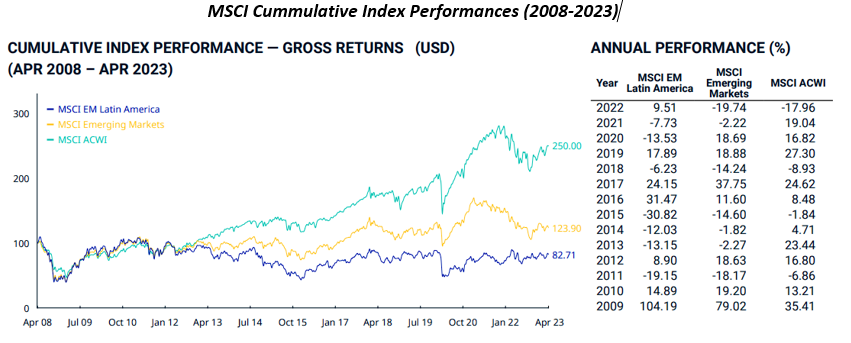

Economic fortunes for the region can fluctuate with natural resource prices. Between 2001 and 2010, equities in LATAM outperformed MSCI World index in 9 out of 10 years, generating a compounded annual return of 21% in dollar terms vs 4% for MSCI world index. Strong performance of LATAM equities was driven by a strong commodity cycle, which fuelled robust economic growth and healthy trade balances for LATAM economies. The fortune of the region began to decline as commodity prices weakened between 2010-2020, driving under performance in its equity market.

After 2020, the fortune of the region improved again following the global pandemic as aggressive expansionary fiscal policies and collapse of interest rates globally drove up the value of real assets and commodities, benefitting the region.

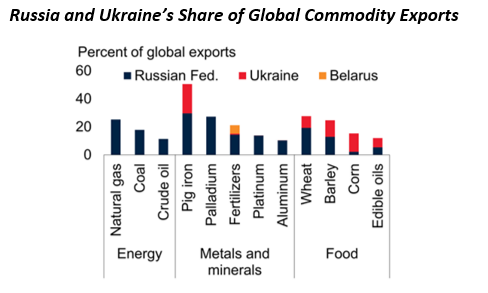

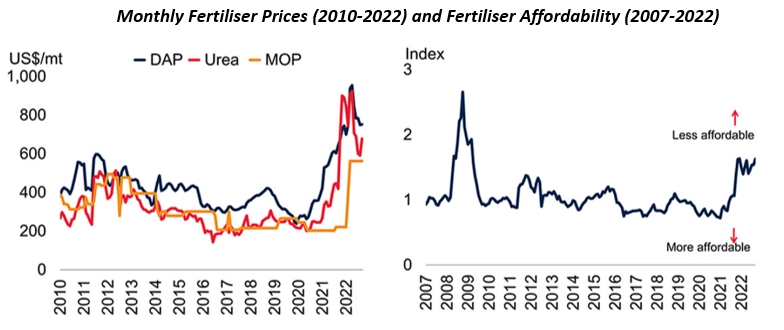

The war in Ukraine perhaps brought into focus the fragility of the food supply system in the world. Russia, Ukraine, and Belarus are significant global suppliers of commodities. These commodities include energy (natural gas, coal), potash (key ingredient in fertilizer), wheat, barley, and corn. The disruption of supply of any of these products has significant implications for consumers across the world.

What is often underappreciated is how different commodities are intertwined. Rising natural gas prices inevitably push up prices for fertilizers, as natural gas is used in the conversion of ammonia to urea for fertilizers. As prices for fertilizers increase, farmers may apply less fertilizer to their crops. Prolonged underapplication of fertilizers reduces crop yield in the future, creating pressure on the security of food supplies.

Source: World Bank

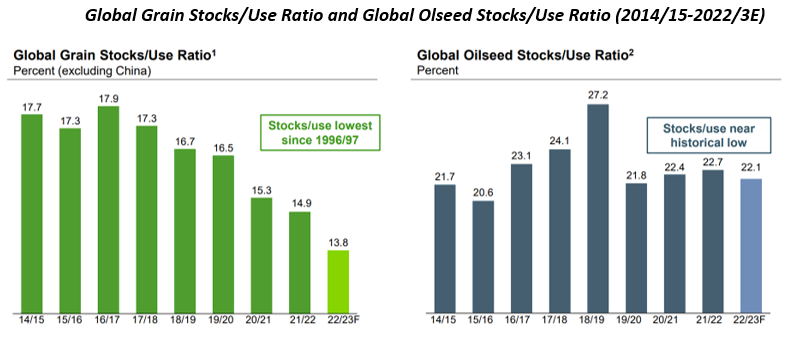

Global grain and oilseed stocks/use ratio hit 25-year lows as supply was disrupted, and global prices for grain and oilseeds (e.g., soybeans, sunflower seeds) rose dramatically. This is not a small issue as they are essential ingredients to almost every person’s diet in the world!

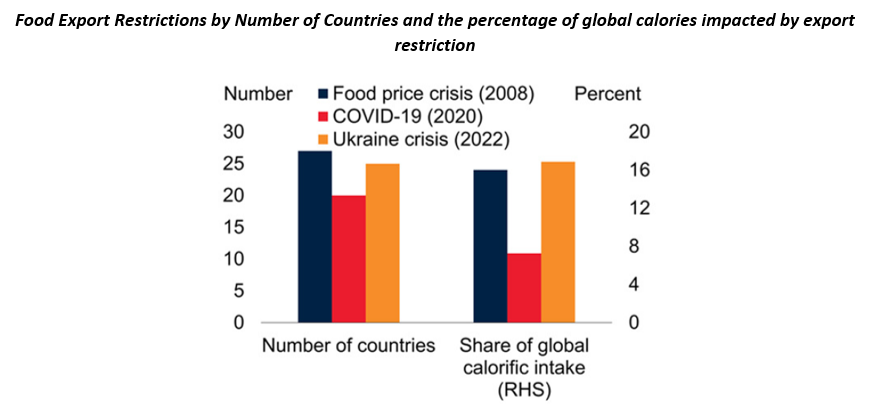

Signs of tightness in the system are already evident. In 2022, many countries started imposing food export restrictions, keeping prices of essential food products low for their own citizens, mirroring what took place in the food price crisis of 2008. The world is perhaps one or two bad harvests or adverse weather events away from a serious food crisis.

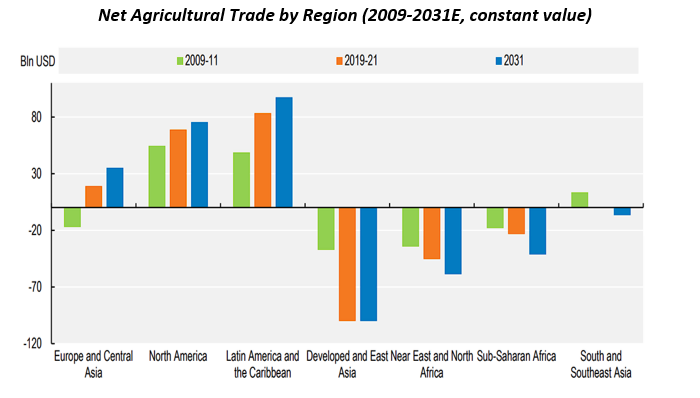

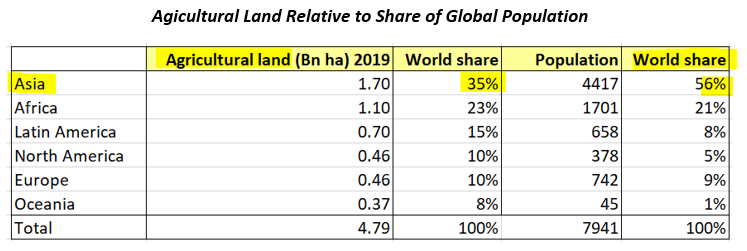

Global demand for agriculture products will continue to grow. There are three key food exporting regions in the world – Europe, North America, and LATAM. In contrast, Asia and Africa are net importers of agricultural products. It is unlikely that the agricultural trade imbalance for Asia can be improved in the coming years, with Asia’s large population base and small share of arable land in the world. The demand from Asia and Africa will continue to grow with economic development, and domestic supply will struggle to keep up as agricultural land makes way for urban developments.

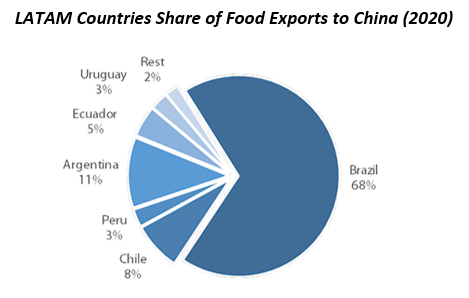

LATAM has a key role to play in this fascinating dynamic, as the need for global food security naturally enhances the region’s strategic importance globally. In particular, Brazil, with the largest mass of arable land in LATAM, is the largest soybean exporter in the world. In 2023, Brazil is also predicted to overtake the US as the largest corn exporter. Global persistent food inflation will negatively impact many economies but will benefit Brazil.

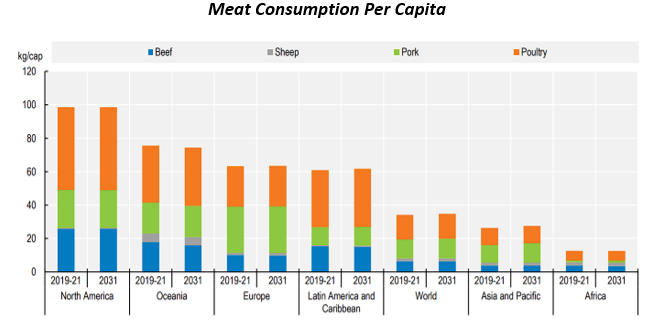

Beyond food security, LATAM will also benefit as the other regions of the world become wealthier. Typically, as countries become wealthier, consumption of meat in their diets increases. At present, meat consumption per capita remains very low in Asia Pacific and Africa. For example, the US consumes 100kg meat per capita, compared with at China, 55kg and India, 5kg. As living standards improve, meat consumption will not only increase, but also upgrade to more lucrative livestock, providing a long runway for beef demand in countries like China.

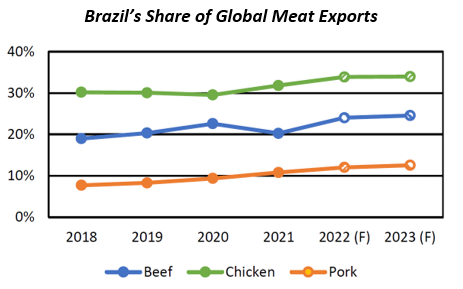

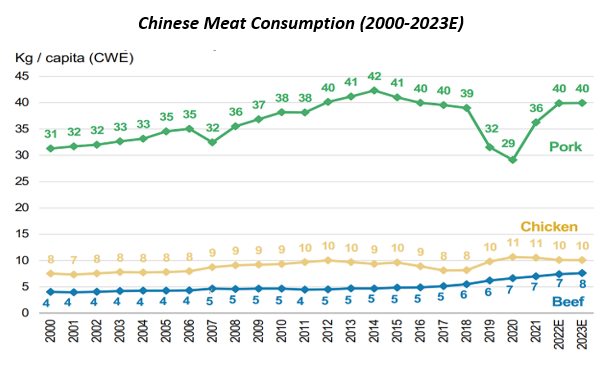

Similarly, to its importance in cultivating some of the world’s most important food crops, Brazil has material export market share in some of the most popular proteins, namely chicken and beef, with over 30% and 20% global market share respectively. Brazil is the largest agricultural exporter to China from the region and notably China’s consumption of Beef has grown consistently from 2000.

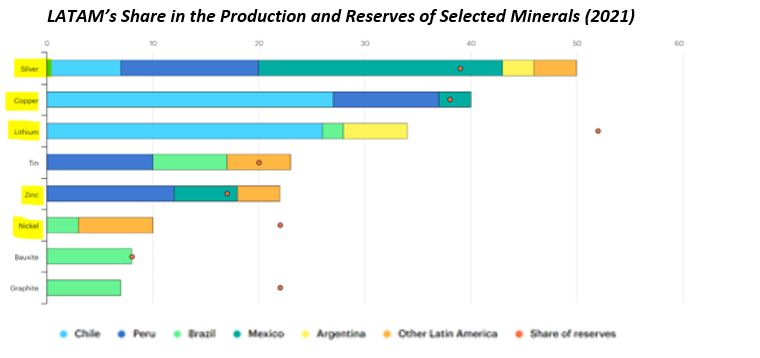

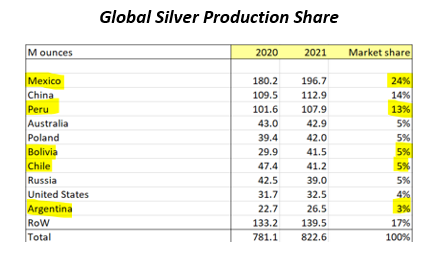

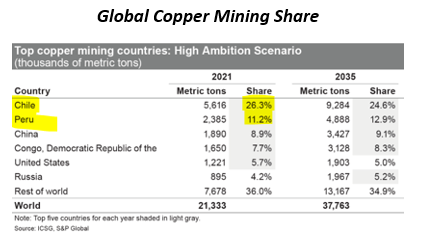

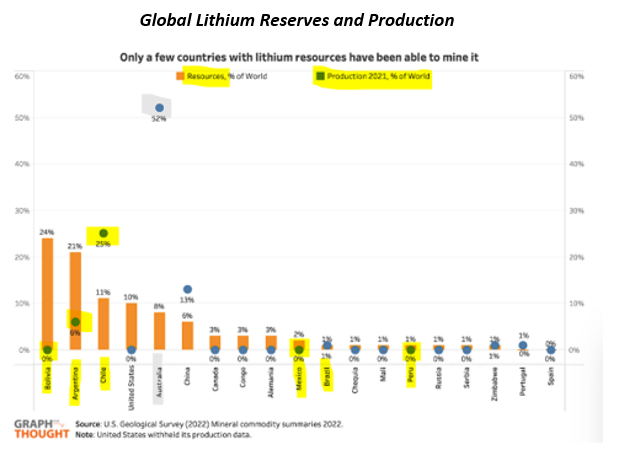

LATAM is also a key producer of critical minerals to the world, including Silver (50%), Copper (40%), Lithium (35%), and Zinc (>20%). Importance of these metals will only grow as these minerals are essential to clean energy transition.

The importance of these minerals in energy transition applications can be a significant long-term tailwind for the mineral rich countries of LATAM, such as Mexico, Peru and Chile.

Furthermore, LATAM controls 60% of lithium reserves in the world, well above its share of current production. In contrast, Australia only has 8% of the world’s lithium reserve, despite currently supplying over 50% of the market. Demand for lithium from the region will likely grow significantly from here.

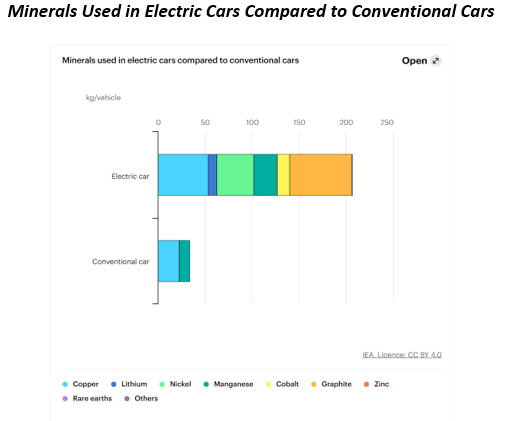

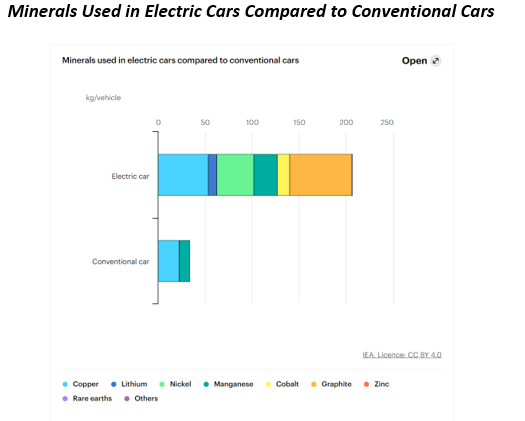

The International Energy Agency (IEA) indicates that a typical electric vehicle (EV) requires six times the minerals of a conventional car, and an onshore wind turbine requires 10x the minerals per MW of a gas-fired power plant. With EV sales expected to grow four times by 2030, and a much wider adoption of wind and solar power generation methods needed to meet global Net Zero targets, largely by 2050-2060, demand for these minerals is also tipped to increase significantly.

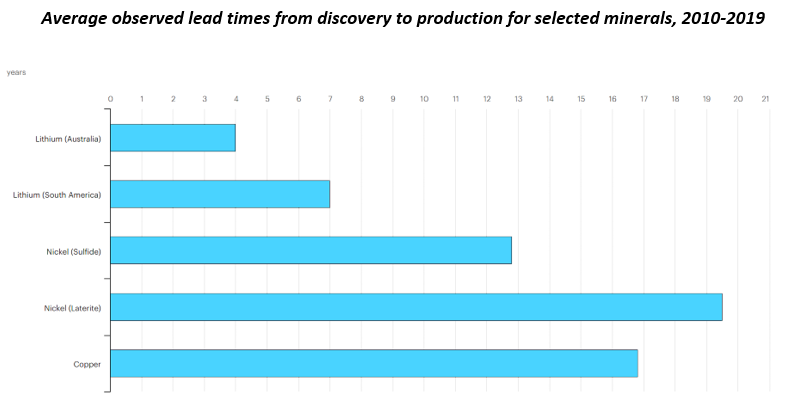

Mining projects take years to develop. Take copper for example, it takes on average over 16 years from discovery to first production. Yet, these minerals are essential for the energy transition. If demand overtakes current supply, it will take a long time to address the supply gap, leading to much higher commodities prices. Many countries in LATAM will benefit tremendously.

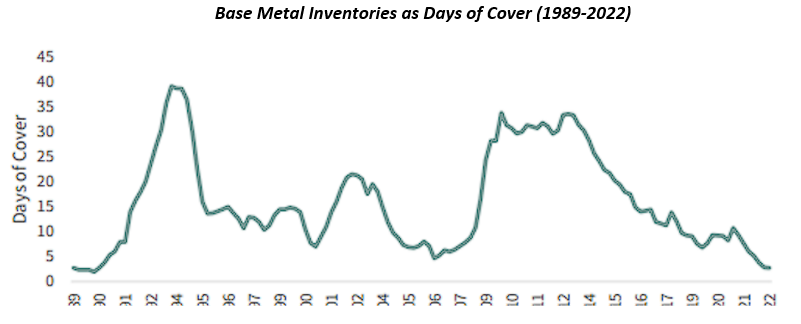

Apart from long lead times in developing new mines, base metal inventories are very low. The chart below tracks the base metal inventories at the major metal trading exchanges. The current exchange inventory level barely covers a few days of global consumption. The current level is already well below the “tightness” levels experienced in 2005/2006. As the world economy expands and the energy transition accelerates, it is only a matter of time before supply and demand shortfalls develop in these important key minerals.

3. Nearshoring- Deglobalisation in the age of Geopolitical Tension

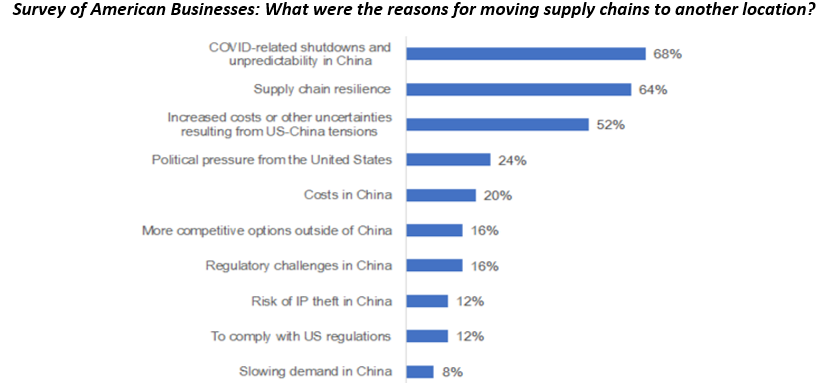

Geopolitical tensions between the US and China are causing businesses and governments to reevaluate where their global supply chains are situated. More and more companies are considering moving their international operations closer to home. Nearshoring is a significant opportunity for the LATAM region in the coming years based on their geographical proximity to North America, and relatively cheap and skilled labour.

Nearshoring could add US$78 billion per annum in additional export revenue in LATAM in the coming years with Mexico being the primary beneficiary, with market share of over 45% or US$35bn of these incremental exports. JP Morgan research estimates nearshoring will boost Mexico’s GDP by 1.2-2.6% per year over the coming five years.

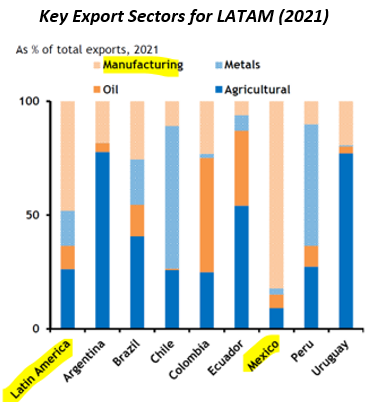

Trade is especially important for Mexico. Unlike its neighbours in the region, Mexico is not as richly endowed with primary resources, making up less than 20% of total exports for Mexico. Instead, Mexico relies heavily on its industrial sectors for exports, with the manufacturing sector representing >80% total exports. The manufacturing sector has grown and matured over the years. Most recently, the top three export categories include auto-components, electronics, and machineries. Mexico is well placed with its long-established export capabilities to fulfil manufacturing orders for an increasing number of international companies.

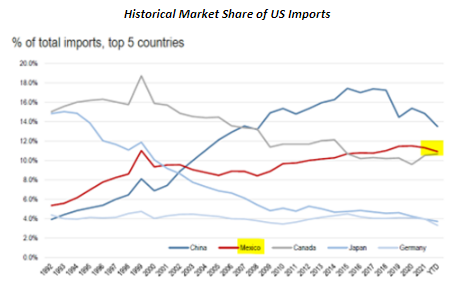

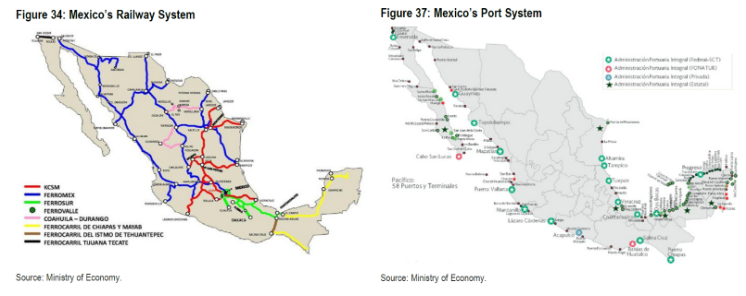

Mexico’s relationship with the US is already well-established, as it is the second largest exporter to the US. Its ~11% share is just behind China’s ~14% and China’s share of imports in the US is in decline. The domestic logistic infrastructure is well developed. Mexico has over 100 airports that have direct flights to-and-from the US and Canada, industrial zones that are connected by over 400km of modern highway, and extensive sea ports along its coast.

Supportive of additional allocation of American MNCs supply chains to Mexico is the availability of a relatively cheap and educated workforce.

The availability of a relatively cheap and educated workforce in Mexico makes it an attractive destination for American MNCs looking to allocate their supply chains.

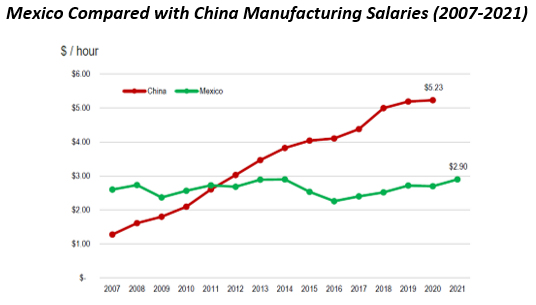

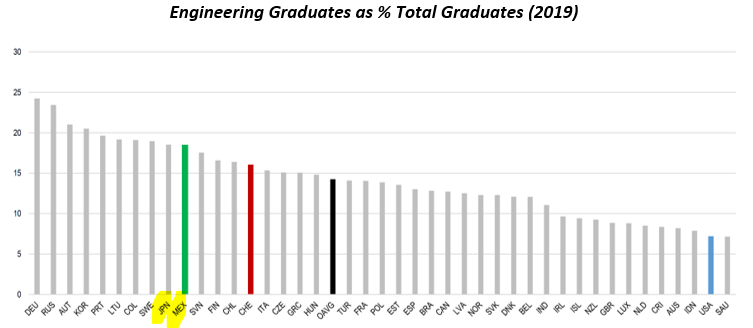

In Mexico, manufacturing wages are much lower than in the US and as much as ~40% lower than in China. Additionally, its workforce is well educated, with a much larger proportion of engineering graduates than even in the US.

Mexico is signatory to 13 free trade agreements with over 50 countries and regions including the US, European Union, Japan, Australia, Canada, Vietnam, and Malaysia and 10 of the 20 countries within the LATAM region. These long-established trade links are increasingly important in the age of geopolitical uncertainty.

4. A Prospective Market Environment

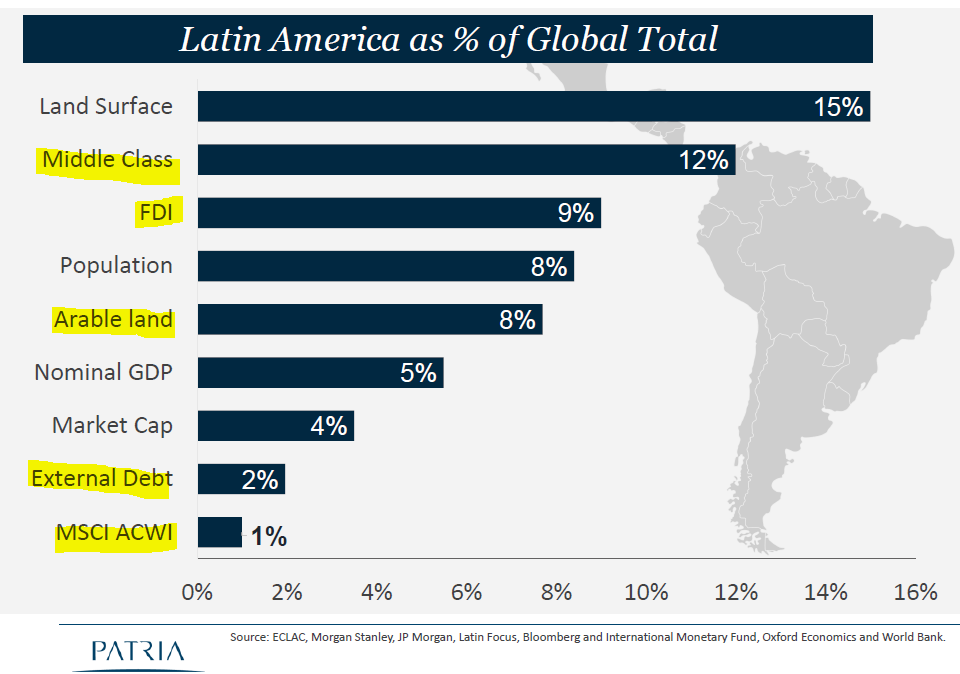

Since 2009, LATAM has under-performed the MSCI world index in nine out of 14 years and the MSCI EM index in 11 out of 14 years. As a result, its index weight in the MSCI world index is now only 1%. In comparison, 12% of the middle-class population of the world lives in the region and the region attracts 9% of global Foreign Direct Investments (FDIs). The potential of the region is seemingly strikingly under-indexed.

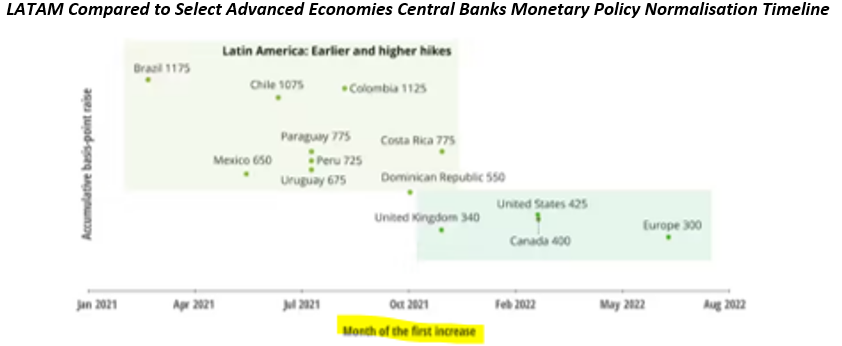

LATAM was not immune to the inflationary pulse of recent years and inflation in LATAM surged to as much as 10-11%. Where the region differed, was that the central banks reacted aggressively much earlier in their fight against inflation in early 2021. In contrast, the UK and US only started to raise interest rates in late 2021 into early 2022.

Despite being further along the tightening cycle and with inflation very likely to have peaked, the policy rate remains very high in LATAM. It is 13.75% in Brazil, 11.25% in Chile and Mexico, and 13% in Colombia. This is in stark contrast to the UK and US where policy rates remain far lower. Inflation across most key countries in LATAM has been brought under control and is expected to decline to 5-6% by the end of 2023 across Brazil, Chile and Mexico, opening the way for significant rate cuts ahead.

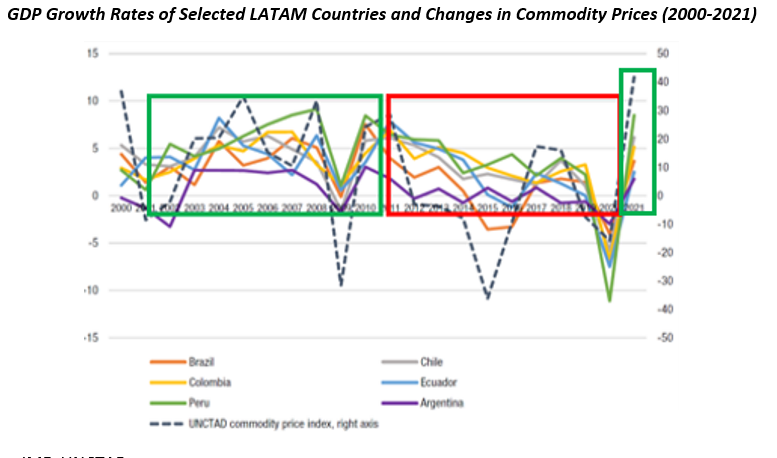

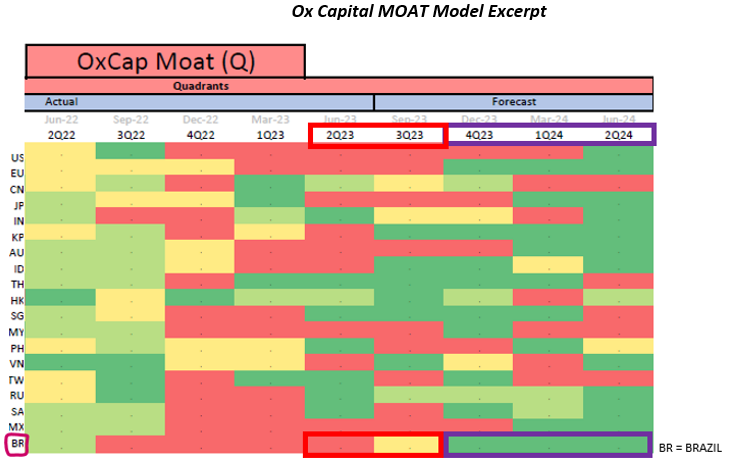

Ox Capital’s proprietary MOAT model suggests the investment climate in the region will improve from 3Q23 onwards (red to purple box below), as falling interest rates support the strengthening of domestic economies.

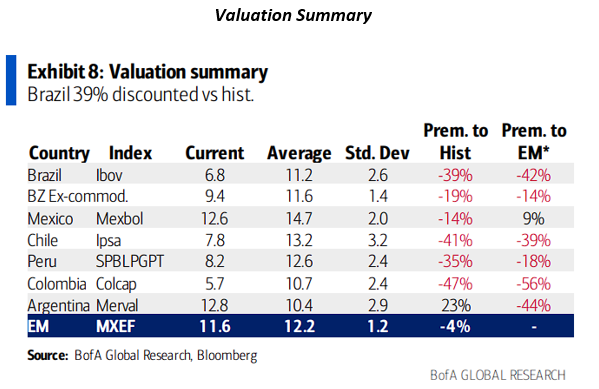

General disinterest in LATAM, along with crushing high interest rates, pushed equity markets in the region into deep discounted territory. The Brazilian market is trading at 6.8X PE, 39% below its historical average of 11X. For Peru, Colombia, and Chile, key commodities nations of LATAM, the current valuation discount is just as steep. By contrast, Mexico has benefitted from nearshoring activities and a buoyant US market over the past few years, and resultantly, is not faring as badly, at 13X PE, a 14% discount to its historical valuation.

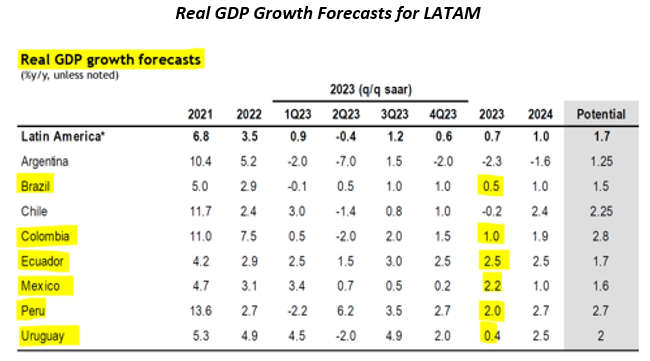

The stock markets in the region appear to be pricing in a dire economic outlook. Yet, most countries in the region are still expected to deliver positive real GDP growth in 2023.

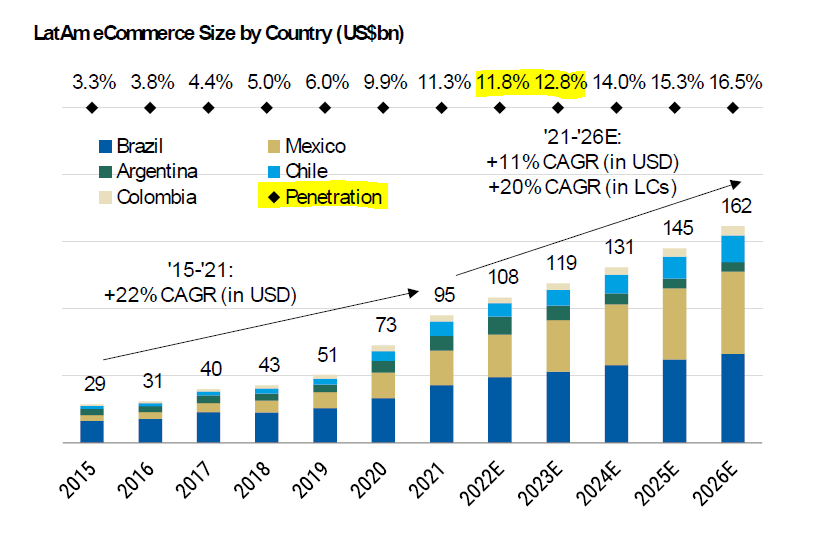

Importantly, as the economies in the region recover, there are many exciting long duration investment opportunities, supported by the expansion of the middle-class and the resulting changes in consumption patterns. E-commerce has a multi-year growth runway, given the low penetration of only 12% in 2022 across the region and improving logistics and incomes. Better healthcare is another long duration opportunity in the coming years. Hospital beds per thousand inhabitants in the region is low compared to the rest of the world and is set to grow. Demand for financial services will also accelerate. In Brazil and Mexico, only 2.3% and 3.6% of the population in these two countries respectively have investment accounts. These figures are well below that of developed countries, as well as China.

5. Conclusion

The past decade has been difficult for markets in the LATAM region. Subsequently, its weighting in the MSCI World Index has dropped to an almost irrelevant 1%. In our view, its market weight substantially under-represents the region’s importance to the world, particularly in the long run.

We believe it it is important for investors to maintain exposure in LATAM as a hedge against an inflationary world. With Brazil’s position as the largest soybean exporter and soon-to-be corn exporter in the world, as well as Chile and Peru’s, leadership in copper production. Mexico is especially well-positioned to be the nearshoring partner of the US, LATAM equities will be increasingly in demand.

The institutions in the region are improving. In fact, the key countries in LATAM are carrying less public debt than some of the major G7 countries. Additionally, their central banks have also shown greater awareness and independence in combating inflation during and following the COVID-19 pandemic.

Current valuations are compressed across the region and provide an attractive entry point for investors. As interest rates are cut in the coming quarters as inflation peaks, economies in the region will regain momentum. Spurred by improving economic activity, structurally growing companies geared towards the rising middle class can benefit greatly from cyclical and structural improvements in the region and this is where Ox is positioned.