Ox on the Ground: The Indonesian Recovery is Underpriced

Debunking the Indonesia “Malaise”: Turning the Taps On in 2026

Indonesia stands at a critical juncture, offering a compelling opportunity for investors who can look past short-term noise to see a rising economic giant. With a population of approximately 285 million and a nominal GDP per capita nearing US$5,400, the nation is at the “sweet spot” where middle-class consumption historically explodes. The potential for GDP to grow multifold from here is supported by a young demographic, with a median age of roughly 30 years, and an economy that has consistently run a trade surplus in recent years, positioning Indonesia as a vital cog in the global supply chain. For those who understand the structural reforms currently underway, the “malaise” of 2025 is not a dead end, but a transition towards a more efficient, high-value economy.

Ox on the Ground: CIO Joseph Lai and Analyst Kate Goodwin visted Jakarta in February 2026. Pictured: Febrio Kacaribu, Director General for Economic and Fiscal Strategy for Indonesia, of the Ministry of Finance

The “Malaise” Debunked: Turning the Taps On

Recent concerns regarding economic “malaise” and government competency are largely symptoms of a political handover. For the past three years, government spending as a percentage of GDP remained low, as the nation went through an election year in 2024, followed by an administration shift from legacy projects to a new “nation-building” framework in 2025.

This handover is now complete, and the fiscal ‘taps’ are being turned on. Funding for this new era will be secured by a step-up in revenue collection and improving natural resource royalties. The shift towards social spending, such as the “Free Meals Program” to feed the under-privileged children, can also bolster long-term productivity by improving the health and educational outcomes of the next generation.

Free Meal Kitchen in Operation

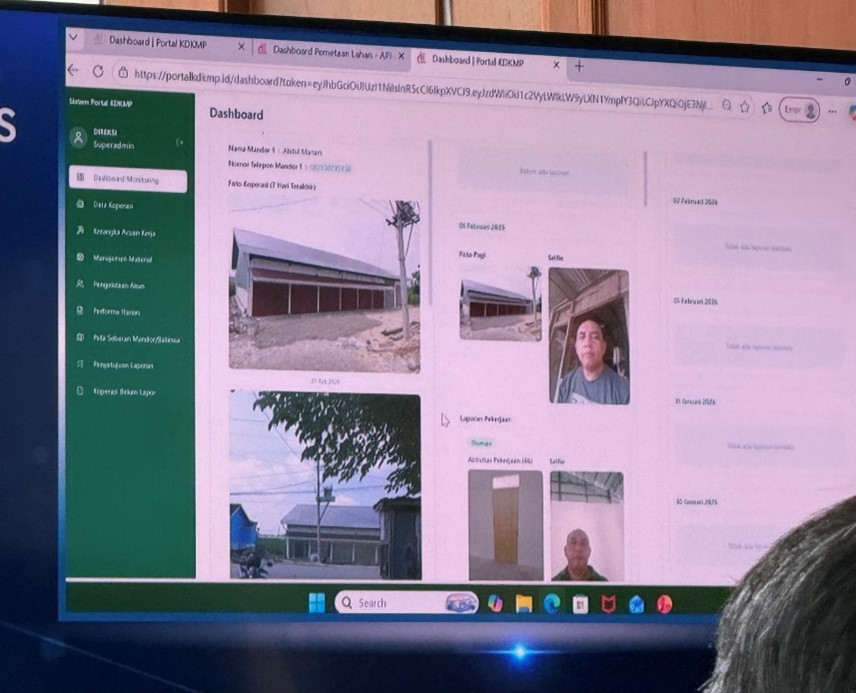

Simultaneously, the government is investing in rural logistics depots under the “Merah Putih Village Cooperatives” program. The village depots are intended to bypass inefficient “rent-seeking” middlemen to deliver much needed products, such as fertilisers and gas to the villages. The construction is monitored by real-time digital dashboards. This level of granular, tech-enabled oversight ensures that capital is spent as intended, rather than lost to corruption.

Ox on the Ground: We viewed the IT Dashboard which is used to monitor each village depot under construction by SOE management. Highly detailed and real-time in nature, this was impressive.

A completed Village Depot

The Danantara Revolution: Institutionalising the “Indonesia Premium”

A significant change is the birth of Danantara, Indonesia’s sovereign wealth fund. Modelled after Singapore’s Temasek, Danantara is tasked with managing roughly US$600 billion of initial assets.

Historically, the Indonesian investment thesis was hampered by a “SOE discount,” where State-Owned Enterprises were forced to balance social missions with commercial viability. Danantara is eliminating this dichotomy by shifting the mandate towards return on investment (ROI) and operational efficiency:

- Asset consolidation: by targeting the amalgamation of over 1,000 disparate state entities into a streamlined group of approximately 200-300.

- Dividend engine: this means a shift towards higher dividend payout ratios. Heavyweights like Bank Negara (BBNI) and Bank Mandiri (BMRI) are now managed to maximise cash flow, providing attractive yields.

- Active stewardship: Danantara acts as an “active owner,” improving cost structures and ensuring capex is directed towards the most productive sectors to meet the government’s 2026 growth targets. Some of the government’s capex will likely be undertaken by the SOE sectors, boosting growth.

Conclusion: The Recovery is Underpriced

The opportunity of Indonesia is currently hidden behind a veil of handover-phase volatility. We are witnessing the professionalisation of the state sector, better monetisation and monitoring of national resources, and a recovery that is already outperforming forecasts. The government programs appear well thought-out, and execution quality is picking up. With blue chip valuations still at attractive levels, the window to capture this multifold growth story is open. Ox Capital is adding to our holdings in these high quality companies in Indonesia.

At Ox Capital, we are focussed on investing in quality franchises with profitable long-term sustainable growth at attractive entry points. Current valuations are providing lots of interesting opportunities. Let us know if you would like to understand specifically where we are finding the opportunities!

Important Information: This material has been prepared by Ox Capital Management Pty Ltd (Ox Cap) (ABN 60 648 887 914) Ox Cap is the holder of an Australian financial services license AFSL 533828 and is regulated under the laws of Australia. This document does not relate to any financial or investment product or service and does not constitute or form part of any offer to sell, or any solicitation of any offer to subscribe or interests and the information provided is intended to be general in nature only. This should not form the basis of, or be relied upon for the purpose of, any investment decision. This document is not available to retail investors as defined under local laws. This document has been prepared without taking into account any person’s objectives, financial situation or needs. Any person receiving the information in this document should consider the appropriateness of the information, in light of their own objectives, financial situation or needs before acting. This document is provided to you on the basis that it should not be relied upon for any purpose other than information and discussion. The document has not been independently verified. No reliance may be placed for any purpose on the document or its accuracy, fairness, correctness, or completeness. Neither Ox Cap nor any of its related bodies corporates, associates and employees shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of the document or otherwise in connection with the presentation.